In today’s financial system, the decision to finance no longer begins with the numbers. It begins with perception.

Before analyzing balance sheets, ratios or cash flows, banks and investors evaluate an increasingly crucial question: what your name conveys when someone searches for it, analyzes it or interprets it.

“A bank doesn’t just finance numbers: it finances trust.”

Digitization, regulation, and massive access to information have turned reputation into a structural variable of financial risk.

It is no longer an isolated element: it directly influences the cost of capital, access to credit, and the viability of a transaction.

What is financial reputation and how does it influence access to credit?

Financial reputation is the perception of reliability and credibility that a person or company projects in the financial system based on their track record, behavior, and public presence.

It’s not built solely on economic results. It also depends on what emerges when a name is analyzed, the coherence of the discourse, and the digital narrative that solidifies over time.

Today, understanding how it is built reputation on google is key. The results associated with a name have become a first layer of evaluation for analysts, investors, and financial institutions.

“Before looking at your numbers, they often look at your name.”

Why does reputation influence the financial risk of companies and executives?

The financial evaluation model has evolved significantly in recent years. Today, data remains essential, but it is interpreted within a broader context.

These organizations don’t just analyze figures; they also interpret signals. They assess whether there is consistency between what a company communicates and what it projects, whether there is relevant media exposure, or whether certain negative associations are repeated in the digital environment.

When an unfavorable narrative takes hold, the impact is direct: it increases perceived risk . And in finance, perception is not secondary: it is decisive.

“Risk isn’t always in the numbers. Often it’s in the perception.”

How do regulators incorporate reputational risk into financial analysis?

The regulatory approach has broadened its scope beyond purely quantitative variables.

The European Central Bank establishes the need to integrate reputational risk within internal governance, while the European Banking Authority includes it in its lending guidelines.

Globally, the International Monetary Fund (IMF) warns that a loss of trust can amplify vulnerabilities even in organizations with solid foundations.

This change reflects a reality: reputation is no longer an intangible, it is a critical variable in prudential analysis.

How does a negative reputation affect access to financing?

When negative information remains visible and is repeated over time, it ceases to be an isolated event and becomes a narrative.

At that point, the problem isn’t just what happened, but how that information is interpreted in the present. And that interpretation can directly affect funding decisions.

Therefore, in certain contexts, strategies are applied aimed at eliminating Google results that generate a distorted or outdated perception.

It is not about eliminating reality, but about preventing a biased narrative from disproportionately influencing financial analysis.

“The problem isn’t always what you did, but what keeps coming back to haunt you.”

What do banks and investors analyze in a financial reputational due diligence?

Reputational review has been structurally integrated into financing processes.

International organizations such as the OECD emphasize the importance of transparency and institutional coherence as the foundation of investor confidence. Meanwhile, the World Economic Forum warns in its Global Risks Report that the loss of trust consistently ranks among the top global risks for organizations.

This trend confirms that perception is no longer an accessory factor, but a structural element in the assessment of financial risk.

In practice, the analysis is not limited to detecting problems. It seeks to understand if there is a consistent narrative, if there are contradictions, or if certain associations can affect the perception of stability—an approach directly linked to online reputation management.

How does artificial intelligence influence financial reputation and credit risk?

Reputation interpretation no longer depends solely on individuals. Automated systems analyze public information and generate a synthesis that influences decision-making.

Therefore, optimizing how AI interprets information has become a strategic factor, especially in contexts where it is key. Improve your reputation on ChatGPT.

When information is inconsistent, the outcome is also inconsistent. And in that process, AI can reinforce perceptions of risk.

“If the information is inconsistent, the interpretation will be too.”

What impact does reputation have on access to financing and the cost of credit?

The impact is tangible. A damaged reputation can translate into more restrictive conditions, higher credit costs, or even the inability to access financing.

This is not a theoretical issue. In competitive markets, any signal that alters the perception of stability influences the decision.

“In finance, perception doesn’t accompany risk: it multiplies it.”

How to protect financial reputation to improve access to financing?

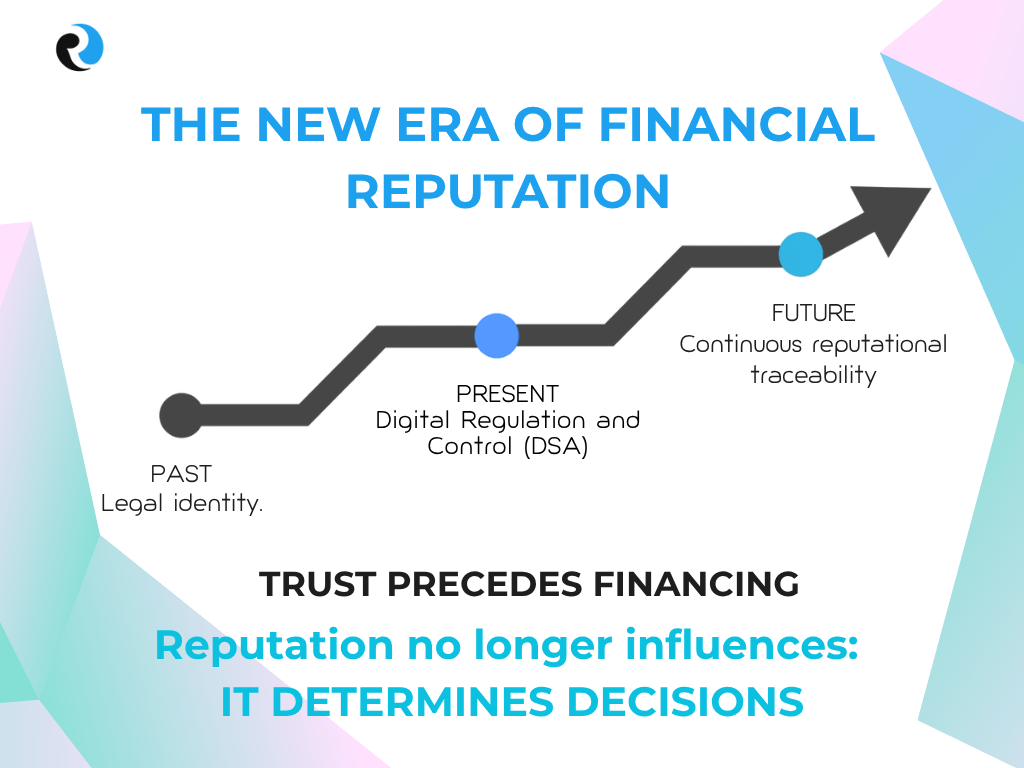

Reputational management should not begin when the problem arises, but much earlier.

It involves identifying risks, building a solid narrative and, when necessary, relying on legal mechanisms such as the right to be forgotten to eliminate harmful information.

The key is not to react, but to anticipate.

“Reputation isn’t repaired in a crisis. It’s built beforehand.”

How does the digital environment and regulation affect financial reputation?

The Digital Services Act has strengthened the traceability of information and the responsibility of platforms.

This has increased the persistence of the information and its impact on public perception.

Today, visibility is not optional: it is structural within modern financial analysis.

Conclusion

Financial reputation is no longer a complement to analysis: it is a structural layer that conditions how data is interpreted.

In an environment where information is accessible, persistent, and analyzed by both people and artificial intelligence systems, perception has become a decisive factor in financial decision-making.

It’s not just about demonstrating solvency, but about projecting coherence, credibility, and control over one’s own narrative.

Because today, more than ever, access to credit depends not only on who you are, but on how you are interpreted within the digital ecosystem.

Frequently Asked Questions (FAQ)

Yes. In modern financial analysis, risk perception includes reputational factors. A negative narrative, even if it doesn’t imply illegality, can influence the terms, approval, or rejection of transactions.

Digital presence, consistency between sources, public history, media mentions and possible negative associations that may affect the perception of solvency and stability.

Yes. Search results are often the first point of verification. They act as an initial layer of validation before in-depth financial analysis.

Yes. Through structured strategies that combine content optimization, removal of harmful information, and the construction of a coherent narrative

It depends on the case, but it generally requires between 2 and 6 months of consistent work, depending on the volume and nature of the existing information.

Because reputation isn’t built overnight. Being proactive significantly improves your standing with banks and investors.